The ethical dimension of insurance sales becomes particularly significant when illness enters the picture.

The ethical dimension of insurance sales becomes particularly significant when illness enters the picture.

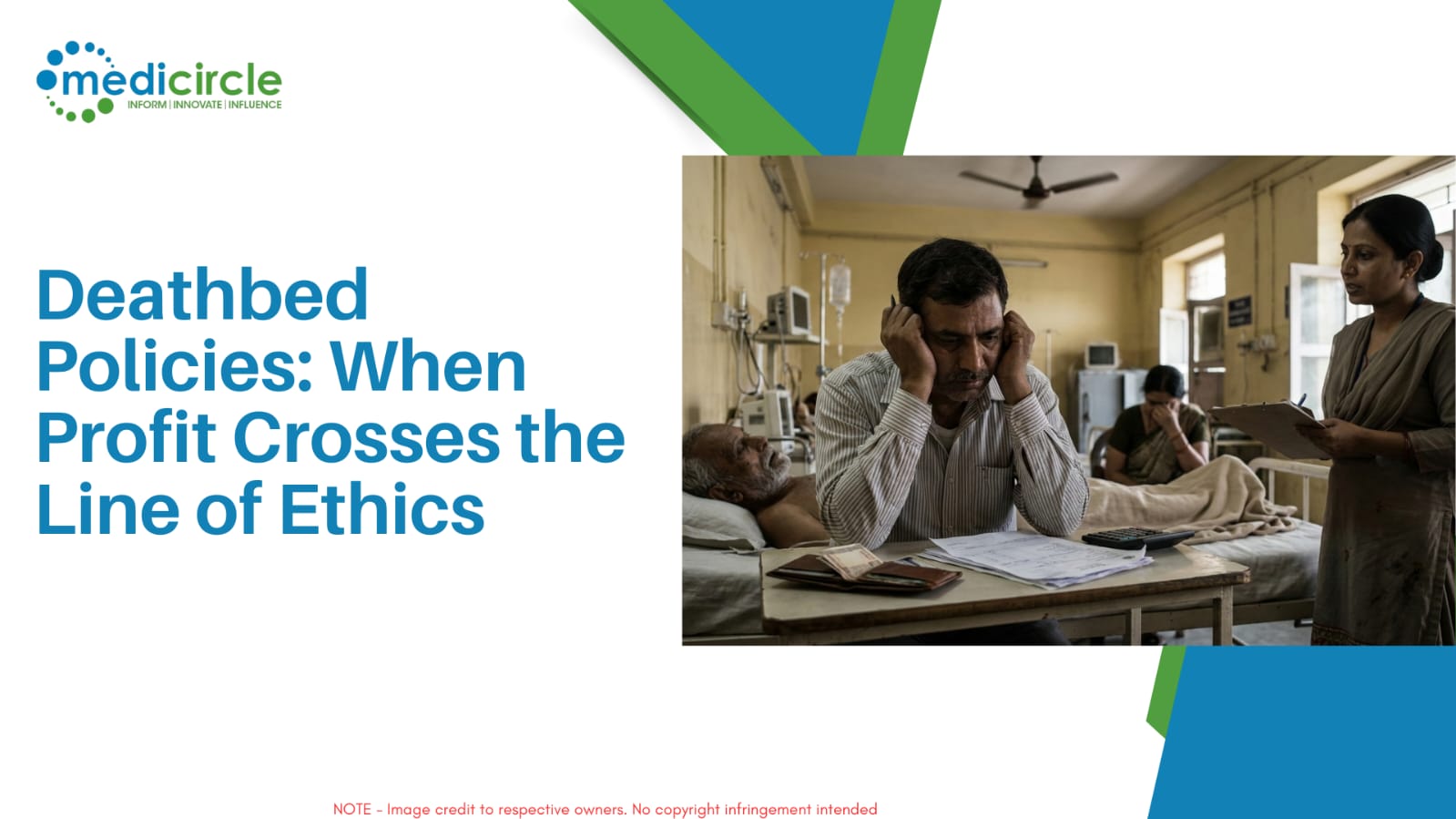

Life insurance was conceived as a shield against uncertainty. It is a promise made in the present to protect families from the financial shock that may follow the loss of a loved one. Across India, millions of households depend on life insurance policies as a safeguard for their future, trusting insurers and agents to operate with transparency and integrity. Yet every so often, troubling allegations surface that shake public faith in this system.

A recent development before the Allahabad High Court has brought to light a deeply disturbing pattern: insurance policies allegedly being issued to individuals who were already critically ill and close to death, sometimes with the involvement of intermediaries who appear to exploit the final days of vulnerable patients. The matter has prompted the court to seek a formal inquiry into the issuance of such questionable policies in the Moradabad region, raising uncomfortable questions about ethics in the insurance sector and the vulnerability of patients and families during medical crises.

Insurance is built on the principle of risk assessment. Before issuing a life insurance policy, companies evaluate a person’s health, age, medical history, and lifestyle. This process helps determine the likelihood of a claim being made in the near future. It is meant to ensure fairness for both the insurer and the insured. When the process functions correctly, it creates a balanced system where families receive financial support while companies manage risk responsibly.

However, when policies are issued to individuals who are already on the brink of death, the entire foundation of insurance underwriting is compromised. Such practices raise the possibility of fraud, misrepresentation, or unethical manipulation of a system designed to offer protection rather than opportunistic gain.

The case that has caught judicial attention emerged during proceedings in which the court encountered multiple instances suggesting that life insurance policies may have been issued under suspicious circumstances. These policies, according to observations placed before the bench, appeared to have been arranged through middlemen at a time when the insured individuals were reportedly extremely ill or near death.

Concerned by the pattern, the court directed the Risk Management Committee Unit in New Delhi to examine the matter and conduct a detailed inquiry in the Moradabad region. The directive reflects the judiciary’s growing awareness of the potential misuse of financial and healthcare-related systems, especially when vulnerable individuals are involved.

Patients who are critically ill often rely heavily on family members, caregivers, and trusted professionals to make decisions on their behalf. During such periods, emotional distress and medical uncertainty dominate daily life. The idea that individuals in such fragile circumstances might be approached or persuaded into purchasing life insurance policies raises profound ethical concerns.

Medical practitioners frequently encounter families grappling with difficult choices at the end of life. Financial pressures can intensify these situations. Hospital bills, medication costs, and prolonged treatment often strain household resources. In this environment, the prospect of financial security through an insurance payout might appear tempting, especially if presented as a quick solution by intermediaries promising immediate policy approvals.

Insurance policies are not designed to function as last-minute financial instruments. Most legitimate policies require medical evaluation, waiting periods, and detailed documentation precisely to prevent misuse. When such safeguards are bypassed or manipulated, the entire regulatory structure begins to weaken.

The inquiry ordered by the court therefore extends beyond a single institution or region. It touches on broader concerns regarding how life insurance policies are marketed, processed, and approved across the country. Regulatory bodies such as the Insurance Regulatory and Development Authority of India have established guidelines to ensure transparency in insurance transactions. These guidelines require clear documentation, proper medical disclosures, and ethical sales practices.

Despite these safeguards, the insurance sector occasionally faces allegations involving forged documents, undisclosed medical conditions, or misleading policy sales. While such cases represent a small fraction of the industry, they can significantly damage public trust.

The Moradabad inquiry may also shed light on the role played by intermediaries in the insurance ecosystem. Insurance agents and brokers serve as the bridge between companies and customers. When they operate responsibly, they guide families through complex financial decisions and ensure that policies align with the client’s needs.

However, if middlemen prioritize commissions over ethics, the system becomes vulnerable to manipulation. In extreme situations, agents may be tempted to push policies onto individuals who are unlikely to qualify under normal underwriting standards. When documentation is fabricated or medical disclosures are concealed, the resulting policies can lead to legal disputes, rejected claims, and financial distress for families.

The court proceedings have also drawn attention to another issue: compliance with judicial orders. During the course of the case, the bench directed the branch head of HDFC Life Insurance Company in Moradabad to appear before the court and clarify certain questions related to service charges and processing fees associated with policy issuance.

When the official did not appear as directed, the court expressed strong displeasure. According to the observations recorded during the hearing, the branch head reportedly communicated with the company’s legal department and suggested that another representative be sent in his place. The court interpreted this action as a failure to comply with its specific instructions.

Judicial accountability is an essential component of regulatory oversight. When courts seek clarification from corporate officials, it signals that the matter carries serious implications. In response to the non-appearance, the bench ordered the issuance of a warrant to ensure the presence of the concerned official in future proceedings. The individual has been asked to explain why contempt proceedings should not be initiated for failing to comply with earlier orders.

While the legal process continues, the larger issue remains the potential misuse of insurance policies involving terminally ill individuals. Such allegations raise questions that go far beyond paperwork or administrative oversight. They challenge the moral boundaries of financial services operating within the sensitive context of healthcare and human vulnerability.

Doctors, nurses, and hospital administrators frequently witness the emotional turmoil experienced by families confronting serious illness. In such circumstances, medical institutions must remain vigilant about the presence of external agents offering financial products that may not serve the patient’s best interests.

Many hospitals already enforce policies restricting unsolicited marketing within medical facilities. These policies exist to ensure that patients and families can focus on treatment decisions without facing commercial pressure during moments of crisis. The allegations highlighted in the Moradabad case reinforce the need for such safeguards.

Financial literacy also plays a vital role in preventing exploitation. When individuals understand how insurance policies work, they are better equipped to recognize unrealistic promises or suspicious offers. Educational initiatives by insurers, regulators, and healthcare organizations can help families make informed decisions about financial planning well before medical emergencies arise.

Another important aspect is the digitization of insurance records and verification systems. Advanced data analytics and centralized databases can help detect irregular patterns in policy issuance. If multiple policies are being approved under unusual circumstances within a particular region or through specific intermediaries, automated alerts can trigger further investigation.

Technology therefore offers a powerful tool for strengthening accountability. However, technology alone cannot replace ethical responsibility. Insurance professionals must remember that their work involves real human lives and real families whose financial stability may depend on honest advice.

The broader insurance industry in India has grown rapidly over the past two decades. Rising awareness about financial planning, increasing healthcare costs, and expanding middle-class aspirations have driven demand for life insurance products. Companies have introduced innovative policies tailored to different stages of life, from child education plans to retirement income schemes.

This growth has largely benefited consumers, offering them new ways to manage financial risk. Yet rapid expansion also brings challenges. Competition among insurers and agents can sometimes create incentives that blur ethical boundaries. Strong regulatory oversight and internal compliance mechanisms therefore remain essential to maintain the integrity of the system.

The inquiry ordered by the Allahabad High Court may ultimately clarify whether the allegations in Moradabad represent isolated incidents or part of a broader pattern requiring regulatory reform. If irregularities are confirmed, they could prompt stricter monitoring of policy approvals and tighter supervision of sales agents.

For families across the country, the case serves as a reminder to approach insurance decisions with caution and awareness. Life insurance should be viewed as a long-term financial safeguard rather than a last-minute financial instrument. Policies taken under pressure or without proper understanding may create more complications than security.

Healthcare professionals often emphasize the importance of planning ahead, whether for medical treatment or financial protection. Insurance works best when individuals purchase coverage while they are healthy and able to provide accurate medical information. This allows policies to function as intended, offering reliable support to families in times of loss.

The ethical dimension of insurance sales becomes particularly significant when illness enters the picture. Patients facing serious medical conditions deserve compassion, dignity, and clear communication. They should never feel pressured into financial decisions during moments when their primary focus must remain on health and family.

The unfolding legal scrutiny is therefore about more than a single dispute. It reflects society’s expectation that institutions handling people’s health, savings, and futures must uphold the highest ethical standards. When questions arise, transparent inquiry becomes necessary to protect public confidence.

For now, the spotlight remains on Moradabad, where investigators will examine documents, interview officials, and determine whether policies were issued improperly. The findings may reveal gaps in oversight or expose individuals who exploited the system. Either outcome will carry lessons for the entire industry.

Ultimately, the purpose of life insurance is to provide security when families face their most difficult moments. Ensuring that this purpose is not distorted by opportunism is a responsibility shared by insurers, regulators, healthcare professionals, and society as a whole. When institutions remain vigilant and ethical boundaries are respected, the protective shield that insurance offers can remain strong, reliable, and worthy of the trust placed in it by millions of families.

.jpeg)

.jpeg)

.jpg)

.jpg)

.jpg)